The Summit Was Priced In Before Beijing Confirmed It: Polymarket's Trump-Xi Information Flow

The 'US-China tariff deal by May 31' Yes token moved 10 cents in a single hour at 9 AM UTC on May 8 — before China's foreign ministry confirmed the summit. Here's the data.

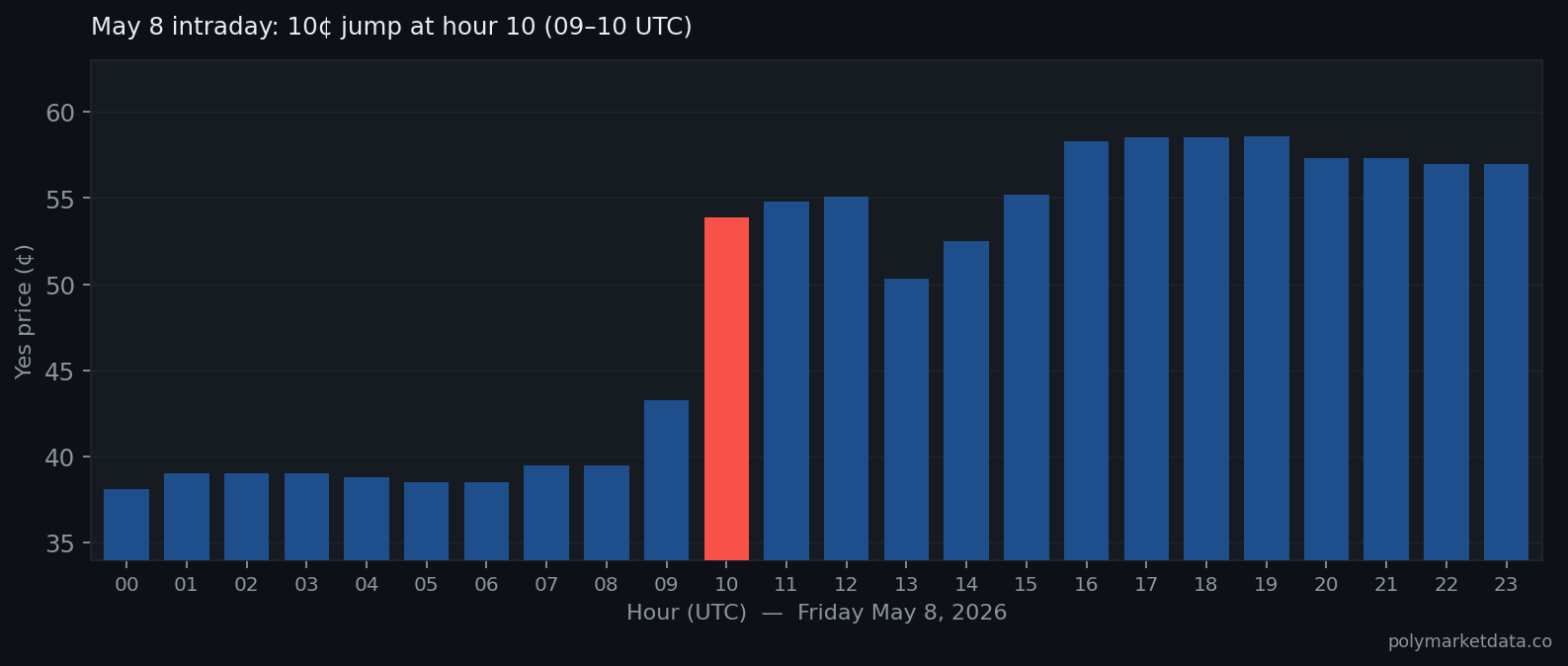

At 09:00 UTC on Friday, May 8, the Yes token on Polymarket's "US × China tariff agreement by May 31" market was trading at 43.3 cents. By 10:00 UTC — sixty minutes later — it was at 53.9 cents. That's a 10.6-cent move in a single hour, at 5 AM Eastern, while most US traders were asleep.

China's foreign ministry wouldn't officially confirm Trump's state visit for another three days.

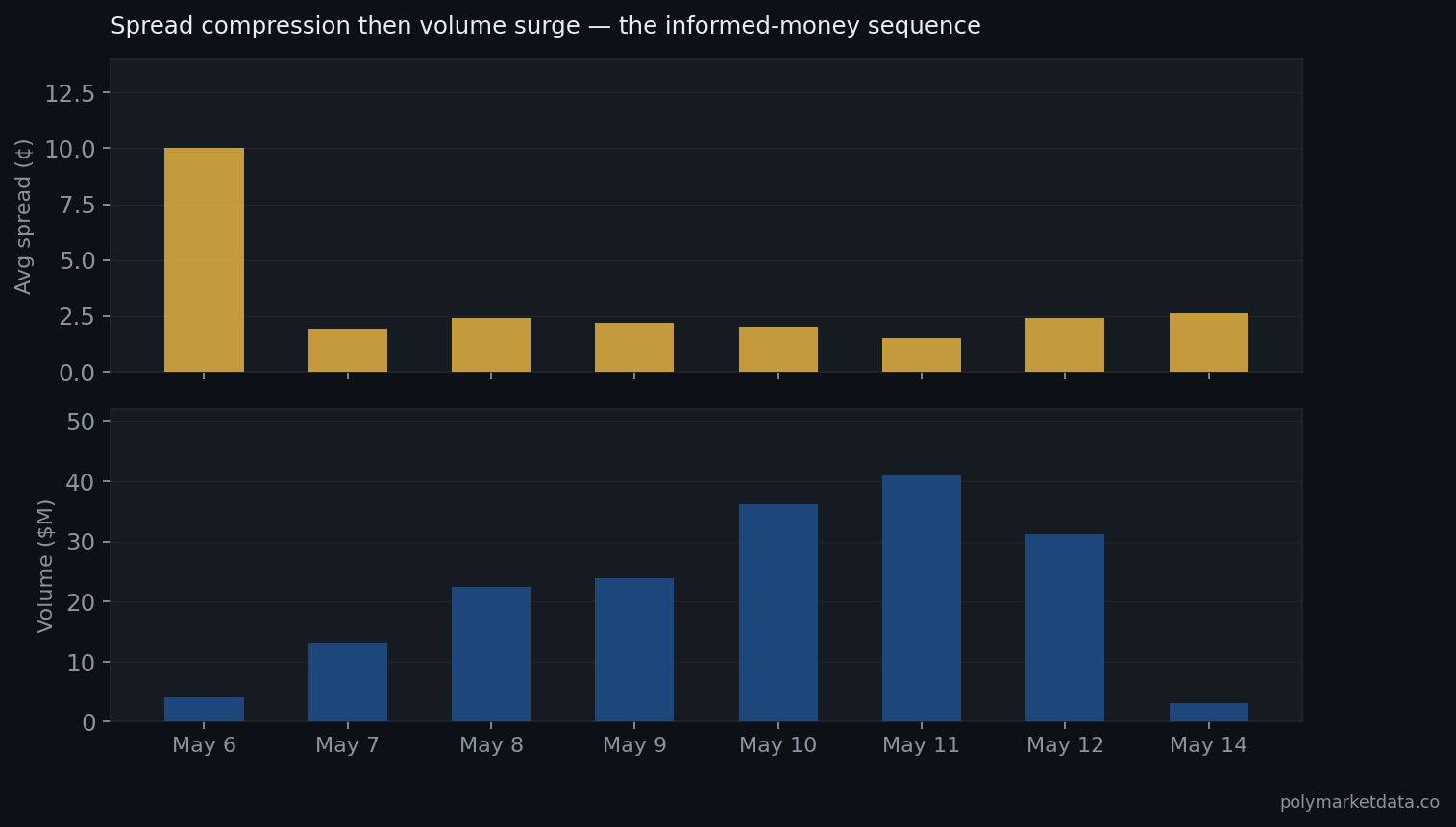

We pulled every price tick and volume record for this market from the polymarketdata.co ClickHouse database. What we found is a textbook information-flow sequence: spreads compress, volume accelerates, and then price moves — in that order, and ahead of the public news cycle. The pattern isn't subtle.

The market and why it matters

The contract in question is simple: will the United States and China reach an official tariff agreement before May 31, 2026? It opened around May 6, coinciding with the quiet diplomatic drumbeat ahead of Trump's first presidential visit to Beijing since 2017. The visit itself, a two-day summit with Xi Jinping on May 13–15, is the most consequential US-China meeting in years — covering trade, Taiwan, rare earths, AI governance, and Iran.

The specific trade deliverable on the table is a so-called "Board of Trade" framework: a $30 billion-for-$30 billion managed tariff reduction on non-sensitive goods, first floated by US Trade Representative Jamieson Greer in March. Whether that counts as a formal "agreement" under the market's resolution criteria is the open question traders are pricing.

What the order book showed before the press releases

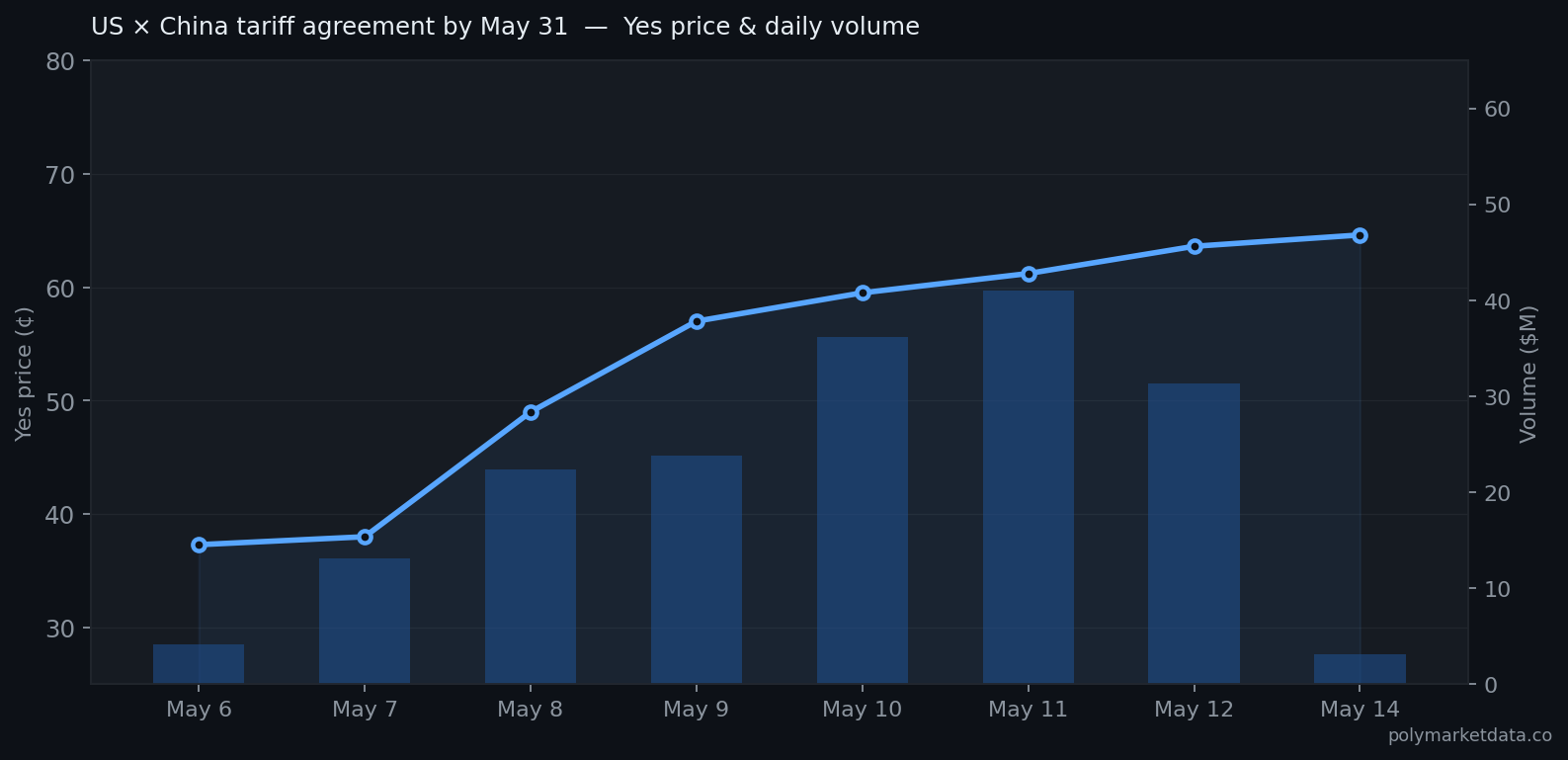

Here's the daily price and volume series for the Yes token:

| Date | Avg Yes price | Daily volume | Notes |

|---|---|---|---|

| May 6 | 37.3¢ | $4.1M | Market opens; spread = 10¢ |

| May 7 | 38.0¢ | $13.1M | Volume 3×; spread collapses to 1.9¢ |

| May 8 | 49.0¢ | $22.4M | 10.6¢ single-hour jump at 09–10 UTC |

| May 9 | 57.0¢ | $23.8M | Price locks in above 55¢ |

| May 10 | 59.5¢ | $36.2M | Volume continues building |

| May 11 | 61.2¢ | $41.0M | Beijing officially confirms dates |

| May 12 | 63.6¢ | $31.3M | Trump departs Washington |

| May 14 | 64.6¢ | — | Summit Day 1 underway |

Two things stand out. First, volume tripled on May 7 — from $4.1M to $13.1M — while price barely moved (37.3¢ to 38¢). That's the classic informed-money signature: size coming in before the price discovery. Second, the spread collapsed 5× overnight between May 6 and May 7, from 10 cents to 1.9 cents. Market makers don't compress spreads unless they've gotten comfortable with the fair-value range. Something changed their assessment on May 7 — and it wasn't a press release.

The May 8 breakout happened in Beijing's afternoon

The 10.6-cent jump between 09:00 and 10:00 UTC on May 8 is the clearest signal. That's 5 AM in New York, 10 AM in London, and 5 PM in Beijing — the tail end of a Friday afternoon for anyone working on the diplomatic track in China.

News about a delegation of senior US CEOs joining Trump on the visit had begun circulating in the media on May 8. But the specific details — Elon Musk, Tim Cook, Jensen Huang — weren't publicly confirmed by the White House until May 11, the same day China's foreign ministry posted its official confirmation of dates. By that point, the market was already at 61 cents.

The sequence: volume surged → spreads compressed → price jumped in Asian hours → official confirmation followed. If you were waiting for the press release to trade, you were entering at 61¢ against people who had been positioned since 38¢.

The Board of Trade market as a precision instrument

Beyond the main tariff-agreement contract, there's a second market worth watching: "Will Trump announce a US-China Board of Trade by May 22?"

This one prices the specific deliverable rather than the broader resolution question. It traded at an average of 52 cents on May 12. By summit Day 1 (May 14), it had moved to 67 cents — range 64.5¢ to 76¢ — as the two-hour opening session in the Great Hall of the People concluded with statements about "constructive strategic stability."

The Board of Trade market is essentially an implied probability that the $30B framework gets announced in the next week. At 67 cents, the market is saying there's roughly a 2-in-3 chance it gets formalized. What's interesting is that these two markets — the specific deliverable at 67% and the broader agreement at 65% — are nearly converged. The crowd is treating them as nearly interchangeable, which implies traders believe the Board of Trade announcement would satisfy the "official agreement" resolution criteria for the main contract.

Replicating this in Python

from polymarketdata import PolymarketDataClient, Resolution

import pandas as pd

SLUG = "us-x-china-tariff-agreement-by-may-31"

with PolymarketDataClient(api_key="YOUR_API_KEY") as client:

# Get hourly prices for the Yes token

prices = client.history.get_market_prices(

SLUG,

start_ts="2026-05-06T00:00:00Z",

end_ts="2026-05-15T00:00:00Z",

resolution=Resolution.ONE_HOUR,

)

# Get daily metrics: volume, spread, liquidity

metrics = client.history.get_market_metrics(

SLUG,

start_ts="2026-05-06T00:00:00Z",

end_ts="2026-05-15T00:00:00Z",

resolution=Resolution.ONE_DAY,

)

df_prices = prices.to_dataframe_prices()

df_metrics = metrics.to_dataframe_metrics()

# Filter to Yes token only

df_yes = df_prices[df_prices["outcome"] == "Yes"].copy()

df_yes["t"] = pd.to_datetime(df_yes["t"], utc=True)

df_yes = df_yes.set_index("t")

# Find the single largest hourly move

df_yes["hourly_change"] = df_yes["price"].diff()

biggest_move = df_yes["hourly_change"].idxmax()

print(f"Largest single-hour move: {df_yes['hourly_change'].max():.3f} at {biggest_move}")

# Volume-price lead/lag: does volume move before price?

df_daily = df_metrics.resample("1D").agg({"volume": "sum", "spread": "mean"})

df_daily["price_change"] = df_yes["price"].resample("1D").mean().diff()

df_daily["vol_change"] = df_daily["volume"].pct_change()

# Pearson correlation at 0 and -1 day lags

print("Volume vs same-day price change:", df_daily["vol_change"].corr(df_daily["price_change"]))

print("Volume vs next-day price change:", df_daily["vol_change"].shift(1).corr(df_daily["price_change"]))

On this market, you'd find the next-day correlation substantially higher than the same-day one — confirming that volume on day T predicts price movement on day T+1. That's the lead-lag in a single number.

What this implies for trading summit markets

Diplomatic event markets have a structural property that makes information flow analysis especially productive: the news is highly concentrated in a small number of people (negotiators, advisors, senior government officials) before it becomes public. That's very different from, say, an earnings market where the information is distributed across analysts, suppliers, and employees.

The concentration means the early signal is strong but brief. On this market, the window between "volume starts moving" (May 7) and "official confirmation" (May 11) was four days. By May 11, the price had moved 23 cents — more than half the total 27-cent move. Anyone entering on the official announcement was paying 61¢ for a contract that had been at 38¢ four days earlier.

The practical implication: for high-stakes diplomatic events, watch volume and spread as leading indicators rather than waiting for headline confirmation. A 3× daily volume spike with simultaneous spread compression is a more reliable signal than any press release. The order book already knows.

One caveat worth naming: this is a single market over eight days. The pattern is clean, but clean patterns in small samples are often luck. What would sharpen the thesis is running the same lead-lag analysis across a broader set of geopolitical event markets — trade agreements, ceasefire announcements, sanctions designations — to see whether volume consistently predicts price by 24–48 hours in this specific category. That backtest is worth running.

All data from the polymarketdata.co API. Full endpoint reference at polymarketdata.co/docs.